- Home

- About NZDFI

- Our Science

- For Growers

- For Wood Users

- Library

- Contact

Other potential markets

We have also identified a range of other potential markets for durable eucalypts, both domestic and international, and worth many millions of dollars annually (see the NZDFI Strategy 2020-2030 document, p5-6). These include high-value indoor and outdoor furniture, interior joinery, cross-arms for power poles, and structural timber.

In terms of exports, a key opportunity for durable eucalypts, especially those with rich colour, is in the substitution of tropical hardwoods such as teak and rosewood. China alone is expected to import 170 million m3 pa hardwoods over next 30 years, and together with India, accounts for some 80% of world tropical log imports. The international market for rosewood is apparently worth more than the trade on ivory, pangolins, rhino horn, lions and tigers put together (e.g. see http://www.unodc.org/unodc/en/data-and-analysis/wildlife.html)

International consumers are already looking for more environmentally sustainable alternatives, and many countries are now limiting imports to timbers produced sustainably. Durable eucalypts will meet these requirements.

Research at the School of Forestry is also looking at the potential for extracting essential oils as a bi-product of eucalypt timber production.

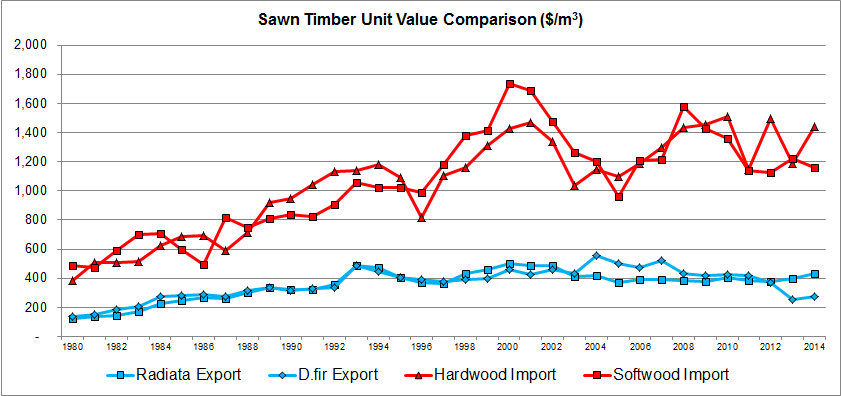

International market opportunity: NZ-grown hardwoods substituting imports

The graph below illustrates the opportunity available to NZ timber growers if they are able to gain access to markets currently supplied by imported timbers. The graph shows the differential between prices received for sawn softwood timber exports (i.e. lumber going over the wharf), and hardwood and softwood lumber imports. The five-year average unit value difference of imported softwood lumber (much of which could be substituted with home-grown durable hardwoods) over exported radiata lumber is some $822 per cubic metre.